Revenue Recognition under ASC 606 | US GAAP Guide, Examples & Journal Entries

Revenue recognition is one of the most critical areas in financial reporting. It directly impacts a company’s profitability, financial position, tax obligations, and investor confidence. Any error or inconsistency in recognizing income can lead to material misstatements, audit qualifications, and regulatory scrutiny.

Under US GAAP, the framework for recognizing revenue is governed by ASC 606 revenue recognition, which provides a structured and principle-based approach. This model ensures that earnings reflect the actual transfer of goods or services to customers.

In practice, many organizations rely on financial reporting and bookkeeping services or professional accounting support to ensure accurate implementation of revenue recognition GAAP requirements.

What is ASC 606 under US GAAP?

ASC 606, Revenue from Contracts with Customers, establishes a single, comprehensive model for US GAAP revenue recognition. It replaces multiple industry-specific standards and introduces consistency, comparability, and transparency.

The core principle of revenue recognition ASC 606 is:

Revenue should be recognized when control of goods or services is transferred to the customer, in an amount that reflects the consideration the entity expects to receive.

This ensures that reporting aligns with economic substance rather than just cash flow timing, forming the foundation of revenue recognition 606 practices.

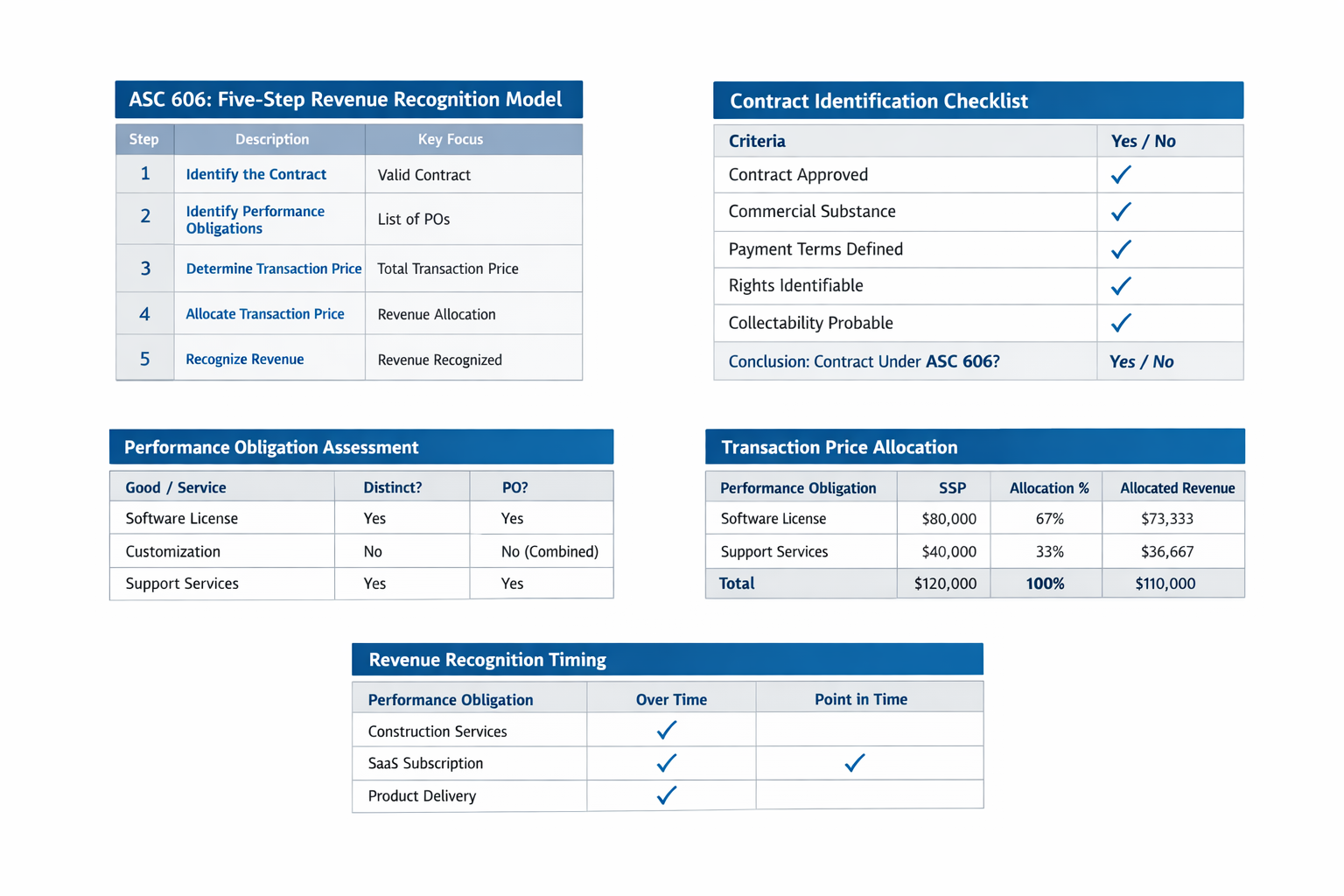

The Five-Step Model for Revenue Recognition

The application of ASC 606 follows a structured framework commonly referred to as the five-step model or ASC 606 steps. These steps require professional judgment, proper documentation, and consistent application.

Organizations often seek revenue recognition consulting services to implement this framework effectively.

Step 1: Identify the Contract with a Customer

Recognition begins only when a valid contract exists. The contract may be written, oral, or implied, but must meet the following criteria:

- Both parties have approved the agreement

- Rights and obligations are clearly defined

- Payment terms are identifiable

- The contract has commercial substance

- Collection of consideration is probable

If these conditions are not met, income cannot be recorded and any amount received is treated as a liability (deferred revenue).

Step 2: Identify Performance Obligations

A performance obligation is a promise to deliver a distinct good or service to the customer. If goods or services are highly interrelated, they are treated as a single obligation.

This step significantly impacts the timing and pattern of reporting and is essential for accurate ASC 606 revenue recognition.

Step 3: Determine the Transaction Price

The transaction price is the total consideration a company expects to receive. It includes:

- Fixed amounts defined in the contract

- Variable consideration such as discounts, rebates, and incentives

- Adjustments for potential reversals (constraint)

- Financing components, if applicable

- Non-cash consideration

Proper estimation is critical, especially when dealing with uncertainty, to ensure accurate reporting.

Step 4: Allocate the Transaction Price

When a contract includes multiple performance obligations, the transaction price must be allocated based on standalone selling prices.

These prices may be determined using:

- Observable market prices

- Cost-plus margin approach

- Adjusted market assessment

This ensures that income is fairly distributed across each obligation in line with its economic value and supports consistent US GAAP revenue recognition.

Step 5: Recognize Revenue

Revenue is recorded when control of goods or services transfers to the customer.

This can occur:

Over Time

- Customer receives benefits as services are performed

- Asset is controlled by the customer during creation

- No alternative use and enforceable right to payment exists

At a Point in Time

- Ownership transfers

- Goods are delivered

- Risks and rewards pass to the customer

- Customer acceptance is obtained

This step ensures alignment between accounting records and actual business activity under revenue recognition GAAP.

Practical Journal Entries under ASC 606 (Step-by-Step)

Step 1: Identify the Contract with a Customer

At this stage, no revenue is recorded. However, advance payments received before performance begins must be recorded as a contract liability (deferred revenue).

Example: Customer pays $50,000 upfront for services to be delivered over 10 months.

Journal Entry (on receipt of advance):

Dr. Cash 50,000

Cr. Contract Liability (Deferred Revenue) 50,000

This reflects the obligation to deliver services in the future. Revenue cannot be recognized yet because performance obligations are not satisfied.

Step 2: Identify Performance Obligations

Identifying performance obligations does not require a journal entry, but it is critical for accounting documentation. Errors at this step lead to incorrect timing of revenue.

Example performance obligations:

- Software license (distinct)

- Implementation services (distinct)

- Ongoing support (distinct)

No accounting entry is passed at this stage, but the contract accounting memo must clearly document the identified obligations.

Step 3: Determine the Transaction Price

This step involves estimation and judgment rather than immediate accounting entries. Variable consideration directly impacts how much revenue can be recognized.

Example: Contract value is $100,000 including a performance bonus of $10,000 that is not probable.

Transaction price considered = $90,000

(No journal entry is passed, but revenue recognition will be constrained to $90,000.)

Step 4: Allocate the Transaction Price to Performance Obligations

Allocation itself does not trigger an accounting entry, but it determines how much revenue is recognized for each obligation.

Example allocation:

- Software license: $60,000

- Implementation services: $20,000

- Support services: $10,000

Total allocated transaction price: $90,000

This allocation drives all future revenue postings.

Step 5: Recognize Revenue When or As Performance Obligations Are Satisfied

Revenue recognized at a point in time (sale of goods or software license).

Example: Software license delivered to customer.

Journal Entry:

Dr. Contract Liability / Accounts Receivable 60,000

Cr. Revenue – Software License 60,000

Revenue recognized over time (SaaS or service contracts).

Example: $12,000 annual SaaS contract recognized monthly at $1,000.

Monthly Journal Entry:

Dr. Contract Liability 1,000

Cr. Revenue – Subscription Services 1,000

Revenue recognized before billing (Contract Asset).

Example: Services performed worth $25,000 but invoice not yet raised.

Journal Entry:

Dr. Contract Asset (Unbilled Revenue) 25,000

Cr. Revenue – Services 25,000

When invoice is raised later:

Dr. Accounts Receivable 25,000

Cr. Contract Asset 25,000

Variable consideration adjustment (rebates or refunds).

Example: Expected rebate of $5,000 on already recognized revenue.

Journal Entry:

Dr. Revenue 5,000

Cr. Refund Liability 5,000

Manufacturing industry – over-time revenue recognition (WIP scenario).

Example: Custom manufacturing contract value $1,000,000. Costs incurred represent 40% of total estimated costs.

Revenue to be recognized = $400,000

Journal Entry:

Dr. Contract Asset (WIP under ASC 606) 400,000

Cr. Revenue – Long-Term Contracts 400,000

Corresponding cost entry:

Dr. Cost of Goods Sold 280,000

Cr. WIP Inventory 280,000

Finished goods sold at a point in time.

Example: Finished goods sold and delivered for $150,000.

Journal Entry:

Dr. Accounts Receivable 150,000

Cr. Revenue – Sale of Goods 150,000

Cost recognition entry:

Dr. Cost of Goods Sold

Cr. Finished Goods Inventory

Trading goods – principal versus agent accounting.

Example where entity acts as principal:

Dr. Accounts Receivable 100,000

Cr. Revenue 100,000

Example where entity acts as agent (commission income @10%):

Dr. Accounts Receivable 10,000

Cr. Revenue – Commission Income 10,000

Contract modification increasing scope.

Example: Contract price increased by $30,000 and treated as a separate contract.

Journal Entry (upon delivery of additional services):

Dr. Accounts Receivable 30,000

Cr. Revenue 30,000

Year-end ASC 606 cutoff adjustment.

Example: Revenue billed but performance obligation not yet satisfied.

Journal Entry:

Dr. Revenue

Cr. Contract Liability

Industry Applications of ASC 606

- Healthcare: Recognized upon service delivery with adjustments

- Real Estate: Point-in-time or over-time recognition

- SaaS & IT: Subscription-based over time

- Manufacturing: Based on customization and delivery

- Trading: Recognized upon transfer of control

Consequences of Non-Compliance

Failure to follow ASC 606 revenue recognition can result in:

- Financial misstatements

- Audit issues

- Regulatory penalties

- Tax inaccuracies

- Loss of investor confidence

Disclosure Requirements

Companies must disclose:

- Revenue breakdown

- Contract assets and liabilities

- Performance obligations

- Key judgments and estimates

Many businesses rely on outsourced accounting and compliance solutions to manage these disclosures effectively and maintain proper US GAAP revenue recognition.

How Unified Books Supports ASC 606 Compliance

Implementing revenue recognition ASC 606 requires technical expertise and structured processes.

Unified Books provides:

- Contract analysis and structuring

- Performance obligation identification

- Allocation and reporting support

- Journal entry preparation

- Audit-ready documentation

Their expertise ensures accurate, compliant, and reliable financial reporting aligned with revenue recognition GAAP standards.

Frequently Asked Questions (FAQs)

What is revenue recognition under ASC 606?

It is the process of recording revenue when control of goods or services is transferred to the customer.

What are the five steps in ASC 606?

The ASC 606 steps include identifying the contract, identifying obligations, determining price, allocating price, and recognizing revenue.

Can revenue be recognized before invoicing?

Yes, under US GAAP revenue recognition, it is recorded as a contract asset when performance is completed.

What is the difference between contract asset and liability?

A contract asset arises before billing, while a liability arises when payment is received in advance.

How does ASC 606 impact SaaS companies?

Under revenue recognition 606, revenue is recognized over time, and setup fees are typically deferred.

Why is ASC 606 important?

It ensures accurate, consistent, and transparent revenue recognition GAAP.

Written by